İş ve Sosyal Güvenlik Uzmanı Vedat İlki

İdari Para Cezası Yıllık İzinle İlişkisi Nedir?

(12.06.2026)

İş ve Sosyal Güvenlik Uzmanı Vedat İlki

İdari Para Cezası Yıllık İzinle İlişkisi Nedir?

(12.06.2026)

Evren Özmen

Evren ÖzmenSerbest Muhasebeci Mali Müşavir

Bilirkişi

evrenozmen@ozmconsultancy.com

www.ozmconsultancy.com

Turkey Non-Dom Relocation Guide

Turkey Non-Dom in Brief

Turkey Non-Dom is the commonly used name for the 20-year foreign income tax exemption under Article 20/D of Turkey's Income Tax Law. It is designed for qualifying individuals who become Turkish tax residents and receive eligible foreign-source income. It is not a blanket exemption for every foreign citizen or every payment received from abroad.

Who this guide is for:

Internationally mobile professionals, investors, retirees, founders, and families considering Turkish tax residence and needing a practical roadmap before they move.

Core decision: determine whether each income stream is foreign-source and potentially exempt under Article 20/D, Turkish-source and potentially deductible under Article 89/13, or fully taxable in Turkey.

What Is Turkey Non-Dom?

The Turkey non dom regime is a 20-year foreign income tax exemption for qualifying individuals who become Turkish tax residents. Introduced by Law No. 7582 and codified as Article 20/D of the Income Tax Law (Gelir Vergisi Kanunu), it can reduce Turkish income tax on qualifying foreign-source income to zero for twenty consecutive years.

To use the Turkey non dom tax exemption, an eligible applicant must obtain an Istisna Belgesi (Exemption Certificate-20/D). GVK General Communique No. 333 sets out the application procedure. The application must be submitted to the competent Turkish tax office by 31 December of the year in which the individual first becomes a Turkish tax resident.

The phrase “Turkey non dom” is commonly used to describe this incentive, although Article 20/D is technically a foreign income exemption rather than a separate legal domicile status. Whether an individual qualifies — and whether the exemption remains defensible over the full twenty-year period — depends on nine practical questions. This guide explains each one, then covers the 100% service export deduction under GVK Article 89/13 for active income earned from Turkey.

Key Facts at a Glance

- Legislation: Law No. 7582, GVK Article 20/D

- Duration: 20 years from the date the Exemption Certificate is issued

- Tax rate on qualifying foreign-source income: 0%

- Eligibility: Foreign nationals becoming Turkish tax residents for the first time in 3 years

- Application deadline: 31 December of the year of first Turkish tax residency

- Qualifying income: Foreign-source income taxed in the country where it arose

- Corporate taxpayers: Not eligible — individuals only

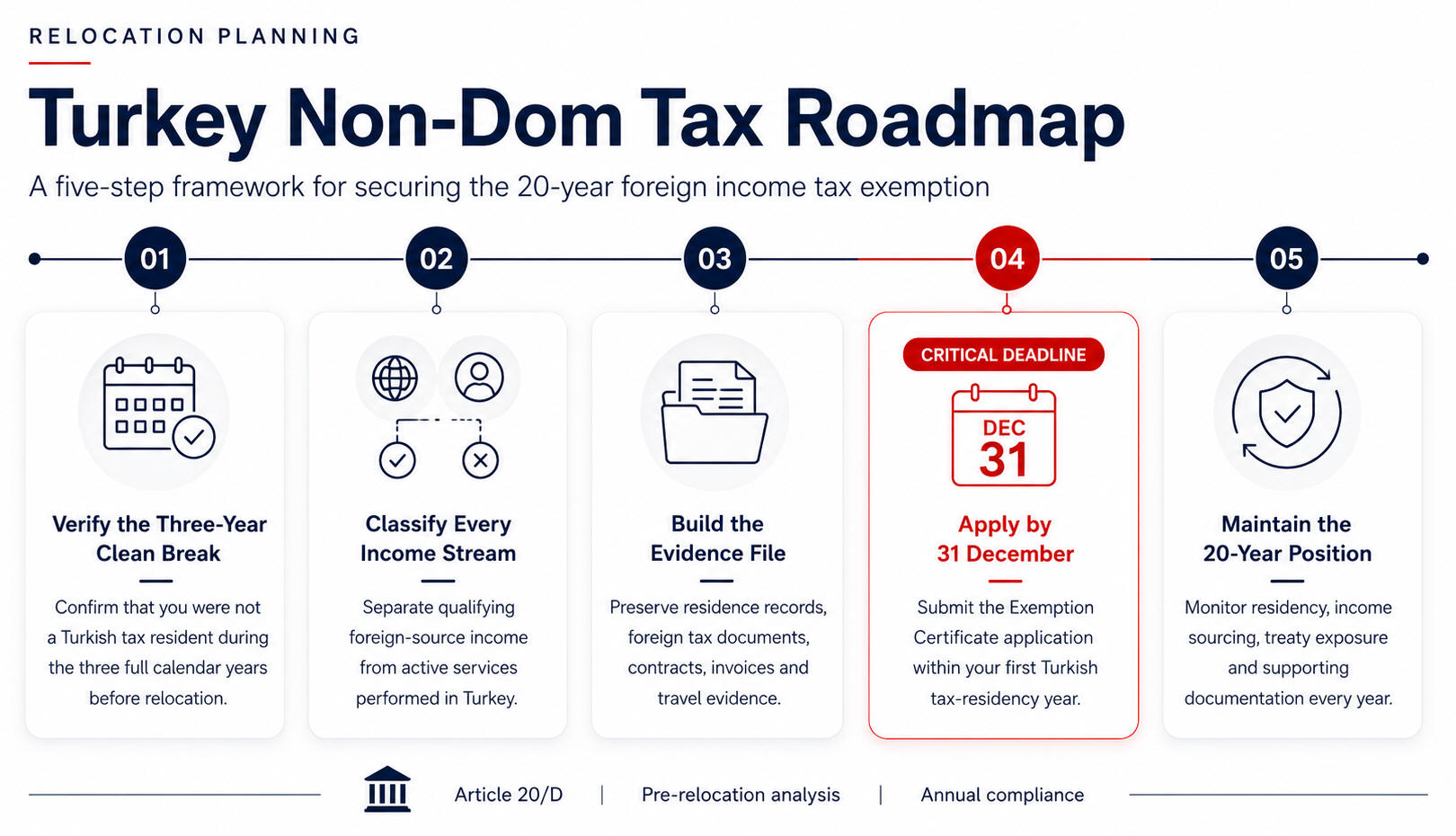

Turkey Non-Dom Relocation Roadmap

The roadmap below moves from initial eligibility screening to annual compliance. Complete the legal and tax analysis before changing residence, signing long-term arrangements, or allowing the relevant calendar year to close.

Phase 1 — 6 to 12 Months Before Moving: Map Your Tax Position

Action: list every income stream, asset-holding entity, citizenship, current tax residence, prior Turkey connection, and expected relocation date. Identify possible exit tax, trailing liability, and treaty issues in the country you are leaving.

Phase 2 — 3 to 6 Months Before Moving: Test Turkey Non-Dom Eligibility

Action: confirm the three-year clean-break requirement, assess Turkish tax residency under both the 183-day and centre-of-life tests, and classify each income stream under Turkish sourcing rules.

Phase 3 — Before Arrival: Design the Income Structure

Action: separate passive foreign-source income from active services performed in Turkey. Review whether Article 20/D, Article 89/13, a tax treaty, or ordinary Turkish taxation applies to each category. Do not assume foreign clients or foreign-currency payments automatically create foreign-source income.

Phase 4 — Arrival Year: Establish Evidence and Apply

Action: preserve travel records, residence evidence, foreign tax documents, contracts, invoices, bank records, and entity documents. Submit the Istisna Belgesi application to the competent tax office by 31 December of the first Turkish tax-residency year.

Phase 5 — First Turkish Tax Return: Separate Exempt, Deductible, and Taxable Income

Action: prepare a documented income-by-income analysis. Claim Article 20/D only for qualifying foreign-source income, claim Article 89/13 only where all service-export conditions are met, and declare Turkish-source or otherwise taxable income correctly.

Phase 6 — Every Year After Relocation: Maintain the Position

Action: monitor tax residence, changes in income structure, treaty exposure, foreign taxes, Turkish-source income, and supporting documentation. Reassess the position before selling assets, changing companies, moving again, or adding Turkish clients.

Turkey Non-Dom Eligibility: 9 Questions to Check Before Relocating

Turkey non dom eligibility depends on more than nationality and a move to Turkey. Each question below addresses a specific condition or structuring risk, and a single wrong answer can eliminate the exemption entirely. Review them before changing tax residence or submitting an application.

Question 1: Do You Meet the Turkey Non Dom Three-Year Rule?

The Turkey non dom regime requires a clean break: you must not have been a Turkish tax resident for the three full calendar years immediately before your year of relocation. This condition is absolute and cannot be waived.

Practical trap: Nufus (population register) address. Maintaining a registered Turkish address does not by itself create tax residency — but it raises the question the tax authority will ask when reviewing your application. Applicants who moved abroad but never formally updated their nufus registration are particularly exposed at the documentation stage.

Question 2: Is Your Income Foreign-Source for Turkey Non Dom Purposes?

Under Turkish domestic sourcing rules, income is sourced where the economic activity generating it is performed — not where the client is located, not where payment originates, and not where the contract is governed.

An individual who relocates to Istanbul and continues providing data analytics, development, or design services to EU clients from an Istanbul apartment is performing those services in Turkey under Turkish sourcing rules. The income is Turkish-source, so the Turkey non dom exemption under Article 20/D does not apply to it.

This is the most common point of failure for digital professionals and remote workers who relocate to Turkey under the assumption that their foreign-denominated income qualifies for the exemption.

Practical trap: GVK General Communique No. 333, Example 10 (Ornek 10) addresses this directly: a software developer who relocates to Turkey and works remotely for a foreign employer from Turkish soil earns Turkish-source employment income. The foreign employer, foreign currency payment, and foreign market orientation are all irrelevant to the sourcing analysis. If this describes your situation, Article 20/D does not protect your active income — but the 100% service export deduction under GVK Article 89/13 may. See the dedicated section below.

Question 3: Can You Meet the Turkey Non Dom Application Deadline?

Missing this deadline permanently eliminates the exemption for that year

The Exemption Certificate (Istisna Belgesi-20-d) application must be submitted by 31 December of the year in which you first become a Turkish tax resident. There are no extensions, no late applications, and no retroactive grants.

An individual who relocates to Turkey in October has approximately ten weeks to gather supporting documentation, identify the competent tax office, and file the application. Where documents must be obtained from foreign tax authorities, translated, and notarised, that window is very tight.

If you became a Turkish tax resident in 2024 or 2025 and did not apply by 31 December of that year, the twenty-year clock did not start. You cannot claim those years retroactively.

Practical trap: The most common error we encounter: individuals who relocate, intend to apply, and then allow the calendar year to close while waiting for a professional opinion that took too long. The cost of that delay is permanent — those exemption years are lost and cannot be recovered under any currently available mechanism.

Question 4: Does Prior Turkish Passive Income Affect Turkey Non Dom Eligibility?

Prior Turkish rental income, investment income, or capital gains do not automatically disqualify an applicant. Article 20/D contains an express carve-out for passive income filings that is widely misunderstood and frequently misapplied by first-pass advisers.

Many applicants with Turkish property or Turkish financial accounts have filed Turkish income tax returns in prior years — typically to declare rental income or dividend income subject to Turkish withholding. A strict reading would suggest that any Turkish tax filing during the three-year lookback period indicates Turkish tax residency and therefore disqualifies the applicant.

That reading is incorrect. The statute expressly contemplates that an otherwise qualifying non-resident may have filed a Turkish return for passive income without becoming a Turkish tax resident for purposes of the exemption. The carve-out is real — but its application requires a factual analysis, not a presumption in either direction.

Practical trap: Most advisers applying a first-pass screening flag any prior Turkish tax filing as disqualifying and decline to proceed. Applicants who were turned away on this basis should seek a second opinion. The carve-out for prior Turkish passive income is a substantive provision, not a technicality, and its correct application has qualified clients who would otherwise have been excluded.

Question 5: Will You Earn Turkish-Source Income After Moving?

The Turkey non dom exemption covers qualifying foreign-source income only. Turkish-source income — including rental income from Turkish property, dividends from Turkish companies, and fees earned by performing services in Turkey for Turkish clients — remains taxable under the applicable Turkish rules and rates.

For individuals with a mixed income base — a foreign investment portfolio alongside a Turkish rental property, or offshore dividends alongside active consulting income earned from Turkish soil — the allocation between exempt and taxable income must be established before the first Turkish annual return is filed.

Entrepreneurs who relocate personally while continuing to operate businesses with Turkish clients or Turkish operations face a further distinction: the exemption protects qualifying personal income. It does not protect income generated by Turkish-connected business activities, and it does not prevent a Turkish permanent establishment analysis from applying to the business itself.

Question 6: Is the Income Personal or Earned Through a Company?

Turkey non dom treatment under Article 20/D is available only to individuals. Corporate taxpayers — including limited liability companies, joint stock companies, and branches — cannot access the regime under any structure.

For entrepreneurs and investors who receive income through a holding company or operating entity, the relevant question is not whether the company qualifies but whether the individual shareholder's personal income — dividends, profit distributions, or capital gains on a share disposal — qualifies as foreign-source income at the personal level.

The answer depends on the company's jurisdiction of incorporation, the nature of the income it distributes, and the sourcing rules applicable under Turkish domestic law and any relevant tax treaty. Relocating personally to Turkey while leaving an operating business in the Netherlands, UAE, or elsewhere requires a clear analysis of what the Turkish-resident individual will actually receive — and in what legal form — before concluding that the exemption applies.

Question 7: Can a Turkish Blue Card Holder Qualify?

Yes they can qualify

Article 20/D refers to 'gercek kisi' (natural persons) without specifying foreign nationality as a criterion, which suggests the regime is accessible to Blue Card holders in principle. Their legal status as foreign nationals under Law No. 5901 supports this reading.

Question 8: Could Exit Tax Reduce the Turkey Non Dom Benefit?

Becoming a Turkish tax resident does not automatically terminate your tax obligations in your prior country of residence. Germany, the Netherlands, the United Kingdom, and Australia each have specific rules — including exit taxes and trailing liability provisions — that apply at the point of departure and in subsequent years.

Germany's exit tax (Wegzugsbesteuerung) under Section 6 AStG is the most commonly encountered issue. It taxes unrealised gains on shareholdings exceeding a ten percent threshold at the moment of departure from German tax residency. If you hold a qualifying stake in a non-German company and relocate to Turkey, Germany may assess tax on the unrealised appreciation — regardless of whether Turkey exempts that income.

Practical trap: A German national who becomes a Turkish non-dom may face income that is exempt in Turkey but fully taxable in Germany — with no available treaty credit. The double tax treaty credit mechanism assumes both countries tax the same income. Where Turkey exempts and Germany taxes, the credit does not apply. This interaction must be analysed and resolved before the move, not after the German assessment arrives.

What Is the GVK Article 89/13 Service Export Deduction?

GVK Article 89/13 allows Turkish tax resident individuals to deduct 100% of income earned from providing services to foreign clients from their Turkish taxable income base, provided four specific conditions are met.

Unlike the Article 20/D exemption, which requires a formal certificate application, the 89/13 deduction is claimed directly on the annual income tax return. However, the taxpayer must be able to substantiate the deduction at audit — documentation is essential.

The Four Conditions for the 100% Service Export Deduction

All four conditions must be satisfied for each qualifying engagement. Failure on any one condition removes the deduction for that income.

Condition 1 — Foreign client: The service must be provided to a person or entity that is neither resident in Turkey nor has a permanent establishment in Turkey. Services provided to Turkish-resident companies or individuals do not qualify, regardless of invoice currency or payment method.

Condition 2 — Performance in Turkey: The service must be performed in Turkey. This is the provision's structural logic: it incentivises skilled professionals to base themselves in Turkey while exporting their output. Services performed abroad for foreign clients fall outside this specific deduction.

Condition 3 — Foreign currency remittance to Turkey: The service fee must be received in Turkey in foreign currency through the Turkish banking system. Payment in Turkish lira — even from a foreign client — does not satisfy this condition.

Condition 4 — Invoice to the foreign recipient: The invoice must be issued directly to the foreign client. Arrangements where a Turkish intermediary invoices the end client and subcontracts to the individual do not satisfy this condition.

How Turkey Non Dom and Article 89/13 Can Work Together?

For a foreign national with a mixed income profile — passive foreign investments plus active client work performed from Turkey — the Turkey non dom exemption and Article 89/13 deduction may operate simultaneously within a single annual tax return.

Example: a relocated professional receives dividends from a Netherlands holding company (passive, foreign-source) and invoices foreign clients directly for consulting services performed from Istanbul (active, Turkish-source by performance). Under this structure, the dividends may qualify for the Article 20/D exemption while the consulting revenue may qualify for the Article 89/13 deduction — subject to satisfying the conditions of each regime independently.

The two regimes do not conflict. They address different income categories through different legal mechanisms. The practical requirement is to maintain clean accounting separation: income claimed under 20/D must be documented as foreign-source; income claimed under 89/13 must be documented as satisfying all four export conditions.

Practical trap: The most common structuring error: a professional relocates, obtains the Article 20/D Exemption Certificate, and assumes that all foreign-denominated income is therefore exempt. Active income earned by working from Turkey for foreign clients is Turkish-source income — it does not fall within Article 20/D. That income must be analysed separately under Article 89/13, or it will be fully taxable at progressive rates of 15 to 40 percent.

Documentation Required to Support the Article 89/13 Deduction

The following documentation should be maintained for each qualifying engagement and retained for the statutory limitation period:

- Signed contracts or engagement letters identifying the foreign client and describing the services

- Invoices issued to the foreign client, denominated in foreign currency

- Bank statements showing receipt of the foreign currency payment in a Turkish bank account

- Evidence of the client's foreign residency or incorporation (company registration, registered address confirmation)

- Where applicable, written confirmation that the client has no permanent establishment or registered presence in Turkey

Turkey Non Dom Frequently Asked Questions

Is Turkey a non-dom country?

Turkey does not use “non-dom” as a formal legal domicile status in the same way as some other jurisdictions. The term Turkey Non-Dom is commonly used for the Article 20/D incentive, which may exempt qualifying foreign-source income of eligible new Turkish tax residents for twenty years.

Who should consider Turkey Non-Dom before relocating?

The regime is most relevant to individuals with clearly documented foreign-source passive income, such as certain foreign dividends, interest, royalties, or capital gains. Remote workers and consultants must analyse active income separately because services performed from Turkey are generally Turkish-source.

What is the most important Turkey Non-Dom deadline?

The key deadline is 31 December of the calendar year in which the applicant first becomes a Turkish tax resident. The Istisna Belgesi application should be prepared early enough to obtain, translate, and notarise supporting documents before that date.

Does owning Turkish property disqualify me from Turkey's 20-year tax exemption?

No. Owning Turkish property does not by itself disqualify an applicant. Turkish rental income from that property is separately taxable in Turkey and must be declared annually. However, prior Turkish rental income declarations do not constitute the disqualifying Turkish tax residency under Article 20/D, provided the declarations arose purely from a passive income obligation. Each case requires factual review.

Can I apply for the Exemption Certificate after I have already moved to Turkey?

Yes, but only within the calendar year in which you first become a Turkish tax resident. The application deadline is 31 December of that year. Individuals who became Turkish tax residents in prior years and did not apply by the applicable deadline cannot claim the exemption retroactively. The twenty-year period begins from the date the certificate is issued.

Does Turkey's 20-year tax exemption cover capital gains from selling foreign shares?

In principle, yes. The exemption covers foreign-source income broadly, including capital gains from disposing of foreign financial assets, provided the income is foreign-source under Turkish domestic sourcing rules and was subject to taxation in the jurisdiction where it arose. Capital gains on shares in non-Turkish companies held by a Turkish-resident individual would generally qualify, subject to treaty analysis and the structure through which the shares are held.

Is Turkey non dom comparable to Portugal's NHR regime?

There are structural similarities. Both create favourable tax treatment for foreign-source income earned by newly tax-resident individuals. Portugal's NHR 2.0, as revised from 2024, offers preferential rates on qualifying income for ten years. Turkey's regime provides a full exemption for twenty years — a longer duration — but applies only to genuinely foreign-source income under Turkish sourcing rules. Turkey imposes no requirement that the income arise from qualifying professional activities. The regimes serve different profiles and interact differently with exit taxation in prior residence countries.

Can my spouse and I both qualify for Turkey's 20-year tax exemption independently?

Yes. The exemption is assessed individually. Each spouse must independently satisfy all eligibility conditions — including the three-year clean break, the foreign-source income requirement, and the 31 December application deadline. Where spouses have different prior residence histories or different income structures, their eligibility analyses may produce different outcomes. Joint applications are not available; each qualifying individual applies separately.

10.06.2026

Kaynak: www.MuhasebeTR.com

(Bu makale kaynak göstermeden yayınlanamaz. Kaynak gösterilse dahi, makale aktif link verilerek yayınlanabilir. Kaynak göstermeden ve aktif link vermeden yayınlayanlar hakkında yasal işlem yapılacaktır.)

>> Duyurulardan haberdar olmak için E-Posta Listemize kayıt olun.

>> SGK Teşvikleri (150 Sayfa) Ücretsiz E-Kitap: hemen indir.

>> MuhasebeTR mobil uygulamasını Apple Store 'dan hemen indir.

>> MuhasebeTR mobil uygulamasını Google Play 'den hemen indir.

>> YILIN KAMPANYASI: Muhasebecilere Özel Web Sitesi 1.666 TL + KDV Ayrıntılar için tıklayın.

Asgari Ücret 2026 - Asgari Ücret Ne Kadar?

Asgari Ücret 2026 - Asgari Ücret Ne Kadar?

Vergi Dilimleri 2026

Vergi Dilimleri 2026

-

İdari Para Cezası Yıllık İzinle İlişkisi Nedir?

İdari Para Cezası Yıllık İzinle İlişkisi Nedir?

-

UYGULAMALI MUHASEBE KAYIT REHBERİ KİTABI ÇIKTI

UYGULAMALI MUHASEBE KAYIT REHBERİ KİTABI ÇIKTI

-

Fazla veya Yersiz Vergi Uygulaması

Fazla veya Yersiz Vergi Uygulaması

-

SGK’ya başvurmadan doğrudan dava açılabilir mi?

SGK’ya başvurmadan doğrudan dava açılabilir mi?

-

7582 Sayılı Kanunla Getirilen Vergi Barışı

7582 Sayılı Kanunla Getirilen Vergi Barışı

-

Hobi Bahçelerinde Aidat mı, Hizmet Bedeli mi? Tahsilatın Gerçek Niteliği Neden Önemli?

Hobi Bahçelerinde Aidat mı, Hizmet Bedeli mi? Tahsilatın Gerçek Niteliği Neden Önemli?

-

7518 Sayılı Yasa İle Türkiye’de Dijital Varlıkların Hukuki Çerçevesi, Genel Kavramlar, Kripto Varlık Hizmet Sağlayıcılığı İle MASAK Denetimi Yükümlülükler ve Vergilendirme

7518 Sayılı Yasa İle Türkiye’de Dijital Varlıkların Hukuki Çerçevesi, Genel Kavramlar, Kripto Varlık Hizmet Sağlayıcılığı İle MASAK Denetimi Yükümlülükler ve Vergilendirme

-

Kart, Şifre ve Kod Satışları ile Diğer Satışlara Aracılık Hizmetlerinden Alınan Bedellerde KDV Uygulaması

Kart, Şifre ve Kod Satışları ile Diğer Satışlara Aracılık Hizmetlerinden Alınan Bedellerde KDV Uygulaması

-

Gelir vergisinin yarı-tam mükellefleri

-

İlamsız Takipte Peşin Harç Her Durumda Yanar mı?

İlamsız Takipte Peşin Harç Her Durumda Yanar mı?

-

Varlık Barışında Tartışmalı Soru: Türkiye’de Alınan ABD Hisseleri Varlık Barışına Konu Olabilir Mi?

Varlık Barışında Tartışmalı Soru: Türkiye’de Alınan ABD Hisseleri Varlık Barışına Konu Olabilir Mi?

-

Yılın Kampanyası: Muhasebecilere Özel Web Sitesi 1.666 TL + KDV