YMM Ertuğrul Tuncer

YMM Ertuğrul Tuncer

Evren Özmen

Evren ÖzmenSerbest Muhasebeci Mali Müşavir

Bilirkişi

evrenozmen@ozmconsultancy.com

www.ozmconsultancy.com

How to Apply Non Dom Turkey 20 Year Zero Tax?

Turkey has introduced a new tax exemption for certain individuals who become Turkish tax residents. Under Income Tax Law repeated Article 20/D, qualifying real persons may benefit from a 20-year income tax exemption on income and gains earned outside Turkey.

This regime is often described as a Turkey non-dom tax exemption or 20-year zero tax on foreign income, but it is important to understand one point clearly:

the exemption applies only to foreign-sourced income and gains. Turkish-sourced income remains taxable in Turkey.

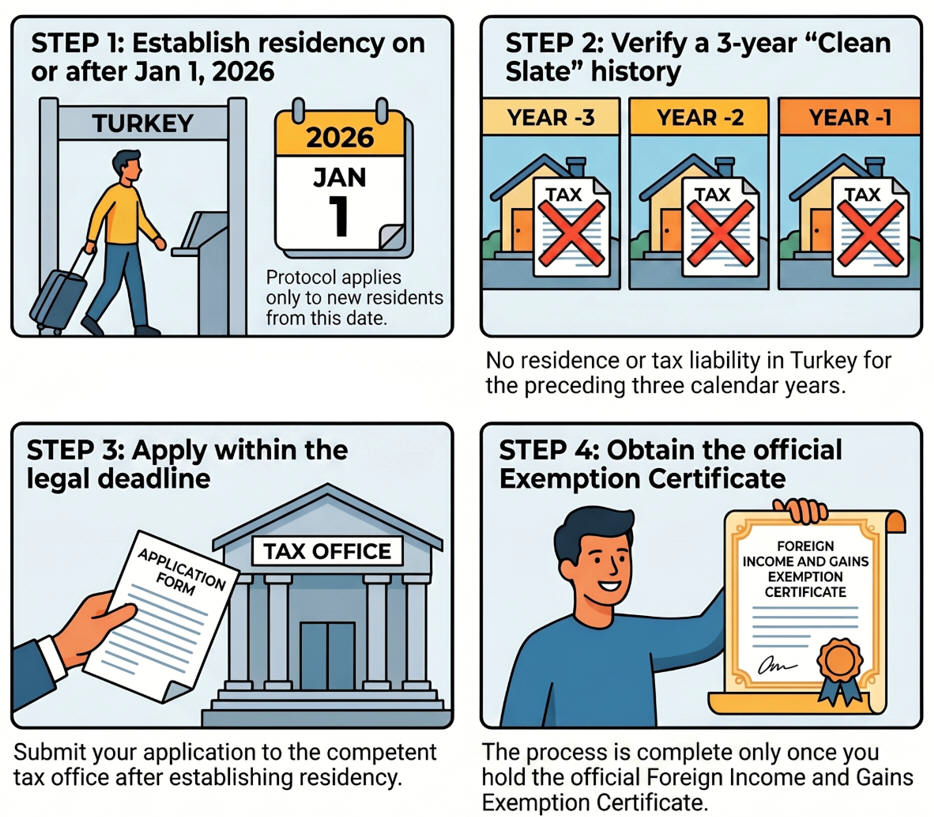

1- Who Can Benefit From Turkey’s 20-Year Foreign Income Tax Exemption?

The exemption is available only to real persons, not companies.

To qualify, the individual must:

- Become tax resident in Turkey on or after 1 January 2026.

- Have had no residence in Turkey during the last three calendar years before becoming Turkish resident.

- Have had no Turkish tax liability during those same three calendar years.

- Apply to the competent tax office within the legal deadline.

- Obtain the official Foreign Income and Gains Exemption Certificate.

In short, the regime targets individuals who move to Turkey after a genuine period of non-residence.

2- What Does “Last Three Calendar Years” Mean?

The three-year test looks at the three full calendar years before the year in which the person becomes resident in Turkey.

For example, if a person becomes resident in Turkey in 2028, the tax office will review whether that person had Turkish residence or tax liability in:

|

Year of Turkish Residence |

Years Checked |

|

2026 |

2023, 2024, 2025 |

|

2027 |

2024, 2025, 2026 |

|

2028 |

2025, 2026, 2027 |

If the person had Turkish residence or disqualifying tax liability in those years, the exemption may be denied.

3- Which Income Is Covered?

The exemption covers income and gains earned outside Turkey by qualifying individuals.

Examples of potentially covered foreign income include:

|

Type of Income |

Covered? |

|

Rental income from foreign real estate |

Yes |

|

Dividends from foreign companies |

Yes |

|

Interest from foreign bank accounts |

Yes |

|

Capital gains from foreign assets |

Yes |

|

Other foreign-sourced income and gains |

Potentially yes |

For example, if a qualifying Turkish tax resident receives dividends from a company resident in Spain or rental income from a property in Monaco, those amounts may fall within the exemption.

4- Which Income Is Outside the Scope?

The exemption does not apply to income earned in Turkey.

Turkish-sourced income remains subject to normal Turkish tax rules.

Examples of income outside the exemption include:

|

Income Type |

Tax Treatment |

|

Rental income from property located in Turkey |

Not exempt |

|

Dividends from a Turkish company |

Not exempt |

|

Salary income earned in Turkey |

Not exempt |

|

Business income from activities in Turkey |

Not exempt |

|

Professional service income from work performed in Turkey |

Not exempt |

A key example is consultancy work. If a person provides consultancy services from Turkey, even to foreign clients, that income may be treated as Turkish-sourced and therefore outside the exemption.

5- Does Previous Turkish Income Always Block the Exemption?

Not always.

The communiqué states that certain passive income tax liabilities before entering the regime do not prevent the individual from benefiting.

The following previous Turkish income types do not automatically block eligibility:

|

Previous Turkish Income |

Blocks Exemption? |

|

Turkish rental income |

No, if other conditions are met |

|

Turkish movable capital income |

No, if other conditions are met |

|

Turkish capital gains |

No, if other conditions are met |

However, other types of Turkish tax liability may block the exemption.

For example:

|

Previous Turkish Income |

May Block Exemption? |

|

Salary income in Turkey |

Yes |

|

Commercial business income in Turkey |

Yes |

|

Professional income in Turkey |

Yes |

6- How to Apply for the Turkey Non-Dom 20-Year Tax Exemption?

To benefit from the exemption, the individual must apply to the competent Turkish tax office and obtain the exemption certificate.

The required certificate is called:

“Yurt Dışından Elde Edilen Kazanç ve İratlar İçin İstisna Belgesi”

meaning:

Foreign Income and Gains Exemption Certificate

7- Application Deadline

The application must be made:

|

Situation |

Deadline |

|

Person becomes Turkish tax resident during the year |

By the end of that calendar year |

|

Person becomes resident in the last two months of the year |

By the end of February of the following year |

For example, if someone becomes Turkish tax resident on 12 July 2026, they must apply by 31 December 2026.

If someone becomes resident in November or December, they may apply until the end of February of the following year.

What Will the Tax Office Check?

The tax office will check whether the applicant:

- Is considered resident in Turkey at the application date.

- Had no Turkish residence in the previous three calendar years.

- Had no disqualifying Turkish tax liability in the previous three calendar years.

- Applied within the legal deadline.

If the conditions are satisfied, the tax office issues the exemption certificate.

8- Is a Tax Return Required for Exempt Foreign Income?

No.

Foreign income and gains covered by the exemption are not declared in the annual income tax return.

If the individual has other taxable Turkish income and must file a Turkish tax return, the exempt foreign income is not included in that return.

9- Can Foreign Taxes Be Credited in Turkey?

No.

If foreign tax is paid on income covered by the exemption, that foreign tax cannot be credited against Turkish income tax.

This is because the relevant income is already exempt from Turkish income tax.

10- Can Expenses Related to Exempt Income Be Deducted?

No.

Expenses and costs related to exempt foreign income cannot be used to reduce taxable Turkish income.

For example, expenses connected with foreign rental income cannot be deducted from taxable Turkish rental income.

11- What Happens If the Conditions Are Later Found Not to Be Met?

If the tax authority later determines that the person did not actually qualify, the unpaid tax may be treated as tax loss.

In that case, the tax office may collect:

- unpaid tax,

- tax loss penalty,

- late payment interest.

This makes proper eligibility analysis very important before relying on the exemption.

12- Does the Regime Apply to Companies?

No.

Only real persons can benefit from this exemption. Corporate taxpayers cannot use the 20-year foreign income exemption.

13- What If the Person Is Not Turkish Tax Resident?

If a person is not tax resident in Turkey, Turkey generally taxes only Turkish-sourced income.

For example, a non-resident individual transferring foreign funds into a Turkish bank account is not taxed in Turkey merely because of the transfer, provided the underlying income is foreign-sourced and the person is not Turkish tax resident.

14- Key Takeaways

Turkey’s new non-dom style exemption may be highly attractive for internationally mobile individuals, investors, retirees, founders, and high-net-worth individuals relocating to Turkey.

The most important points are:

- The exemption lasts for 20 years.

- It applies only to foreign-sourced income and gains.

- Turkish-sourced income remains taxable.

- The applicant must not have had Turkish residence or disqualifying tax liability in the previous three calendar years.

- The application deadline is strict.

- An official exemption certificate must be obtained.

- Companies cannot benefit from the regime.

15- FAQ

Is Turkey offering a non-dom tax regime?

Turkey has introduced a non-dom style exemption for qualifying individuals. It is not identical to classic non-dom systems, but it provides a 20-year Turkish income tax exemption for qualifying foreign-sourced income and gains.

Is foreign income tax-free in Turkey for 20 years?

For qualifying individuals who obtain the exemption certificate, foreign-sourced income and gains may be exempt from Turkish income tax for 20 years.

Is Turkish rental income exempt?

No. Rental income from real estate located in Turkey is not covered by the exemption.

Are foreign dividends exempt?

Yes, foreign dividends may fall within the exemption if the individual satisfies all conditions.

Can Turkish citizens benefit?

The communiqué refers to real persons who meet the conditions. Eligibility depends on tax residence, prior Turkish residence, prior Turkish tax liability, and timely application, not only citizenship.

When should the application be made?

Generally, the application must be made by the end of the calendar year in which the person becomes resident in Turkey. If residence starts in November or December, the deadline is the end of February of the following year.

Is professional income from foreign clients exempt?

If the service is performed in Turkey, the income will be considered Turkish-sourced and outside the exemption, even if the client is abroad.

Kind Regards

05.06.2026

Kaynak: www.MuhasebeTR.com

(Bu makale kaynak göstermeden yayınlanamaz. Kaynak gösterilse dahi, makale aktif link verilerek yayınlanabilir. Kaynak göstermeden ve aktif link vermeden yayınlayanlar hakkında yasal işlem yapılacaktır.)

>> Duyurulardan haberdar olmak için E-Posta Listemize kayıt olun.

>> SGK Teşvikleri (150 Sayfa) Ücretsiz E-Kitap: hemen indir.

>> MuhasebeTR mobil uygulamasını Apple Store 'dan hemen indir.

>> MuhasebeTR mobil uygulamasını Google Play 'den hemen indir.

>> YILIN KAMPANYASI: Muhasebecilere Özel Web Sitesi 1.666 TL + KDV Ayrıntılar için tıklayın.

Asgari Ücret 2026 - Asgari Ücret Ne Kadar?

Asgari Ücret 2026 - Asgari Ücret Ne Kadar?

Vergi Dilimleri 2026

Vergi Dilimleri 2026

-

KDV Beyannamelerinin E-Beyan Sisteminde Verilmesine İlişkin Duyuru Dijital Vergi Dairesinde Yayımlandı

KDV Beyannamelerinin E-Beyan Sisteminde Verilmesine İlişkin Duyuru Dijital Vergi Dairesinde Yayımlandı

-

UYGULAMALI MUHASEBE KAYIT REHBERİ KİTABI ÇIKTI

UYGULAMALI MUHASEBE KAYIT REHBERİ KİTABI ÇIKTI

-

Global Minimum Tax Uygulamasının Ekonomik Etkileri

Global Minimum Tax Uygulamasının Ekonomik Etkileri

-

İnşaat İşlerinde Asgari İşçilik Uygulaması

İnşaat İşlerinde Asgari İşçilik Uygulaması

-

Fason imalatta tevkifat uygulanmasının şartı nedir?

Fason imalatta tevkifat uygulanmasının şartı nedir?

-

Tahakkuk mu, fiili ödeme mi? Tahakkuksa, tahakkuk tarihi ne?

Tahakkuk mu, fiili ödeme mi? Tahakkuksa, tahakkuk tarihi ne?

-

İthalatta Gözetime Tabi Mal Karmaşası! YMM ve Mali Müşavirler İçin Son Tarih 31.07.2026

İthalatta Gözetime Tabi Mal Karmaşası! YMM ve Mali Müşavirler İçin Son Tarih 31.07.2026

-

Transit Ticaret İstisnasında Değişiklikler

Transit Ticaret İstisnasında Değişiklikler

-

KDV İade Taleplerinde İade Edilebilir Azami KDV'nin Tespiti

KDV İade Taleplerinde İade Edilebilir Azami KDV'nin Tespiti

-

TÜRMOB: Yanlış Algıya Karşı Zorunlu Açıklama

TÜRMOB: Yanlış Algıya Karşı Zorunlu Açıklama

-

Fason Olarak Yaptırılan Tekstil ve Konfeksiyon İşleri, Çanta ve Ayakkabı Dikim İşleri ve Bu İşlere Aracılık Hizmetlerinde KDV Tevkifatı

-

Yılın Kampanyası: Muhasebecilere Özel Web Sitesi 1.666 TL + KDV

Yılın Kampanyası: Muhasebecilere Özel Web Sitesi 1.666 TL + KDV