YMM Hasan Aydın

YMM Hasan Aydın

Evren Özmen

Evren ÖzmenSerbest Muhasebeci Mali Müşavir

Bilirkişi

evrenozmen@ozmconsultancy.com

www.ozmconsultancy.com

General Communiqué on Digital Services Tax

How Turkey implement Digital Service Tax ?

Recent development

Turkish Revenue Administration published a draft General Communiqué on Digital Services Tax on 5 February 2020.

Background

As is known, Turkey enacted digital service tax law in December 2019 with a very high tax ratio. Despite digital service tax will enter into force at the beginning of March 2020, there were some doubts about which digital services are included in the scope and how will be the implementation of this tax.

To clarify this doubts Turkish revenue administration published a draft General Communiqué for digital service tax.

What is the scope of digital service tax ?

- Advertising Services rendering in Digital Environment

- Services Related to utilization of digital content and selling audio, visual or digital content

- Running the platforms which users can interact each other in digital environment

- Intermediary services which is rendering in digital environment

What is the registration process for digital service tax ?

Before submitting the first digital service tax statement, digital service providers has to fill the form which located on the website of the revenue administration. (www.digitalservice.gib.gov.tr)

Upon filling and submitting the form which located on www.digitalservice.gib.gov.tr, registration of digital service tax has completed. No physical apply needed. After applying process, password and code will be given to tax payer in order to generate mandatory obligations.

Who are the responsible of digital service tax ?

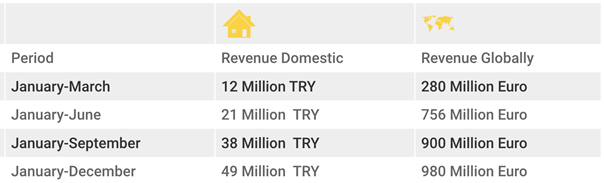

For 2019 period, if the company generate 20 million TRY revenue domestic and 750 million Euro revenue globally will be subject to digital service tax from the beginning of March 2020.

For this company; The digital service tax liability will start from the beginning of October.

If company’ revenues are below 20 million TRY domestic and 750 million Euro globally, to prevent any penalty what should they do ?

They have to submit report from global audit companies which shows their global revenue is below these amounts. Reports do not prepared by audit companies which are not located at least 5 different companies will not be accepted by Turkish authorities.

This audit report has to be translated by sworn translator and must upload to Turkish Revenue administration web page at most on 31 May 2020.

What is the declaration period of digital service tax ?

For digital service tax, the taxation period is one-month periods of the calendar year.

Does this companies has to work with CPA company or notarizing legal books for Turkey ?

No there is no need to notarize any official book or making contract with a CPA company.

What is the ratio of the tax ? What is the tax base ?

Ratio of the tax is % 7,5. Tax base is the whole amount generated in Turkey.

What if company’s do not apply and do not pay the taxes ?

In case the obligations are not fulfilled, Ministry of Turkish Finance & Treasury has a right to block site access until obligations are fulfilled.

With the draft General digital service tax, communiqué Turkish Revenue administration aims to clarify some doubts about digital service tax implementation process for tax payers. I suppose that after some little changes in this draft, it will be published in official gazette within maximum one month.

10.02.2020

Kaynak: www.MuhasebeTR.com

(Bu makale kaynak göstermeden yayınlanamaz. Kaynak gösterilse dahi, makale aktif link verilerek yayınlanabilir. Kaynak göstermeden ve aktif link vermeden yayınlayanlar hakkında yasal işlem yapılacaktır.)

>> Duyurulardan haberdar olmak için E-Posta Listemize kayıt olun.

>> SGK Teşvikleri (150 Sayfa) Ücretsiz E-Kitap: hemen indir.

>> MuhasebeTR mobil uygulamasını Apple Store 'dan hemen indir.

>> MuhasebeTR mobil uygulamasını Google Play 'den hemen indir.

>> YILIN KAMPANYASI: Muhasebecilere Özel Web Sitesi 1.249 TL + KDV Ayrıntılar için tıklayın.

Asgari Ücret 2025 - Asgari Ücret Ne Kadar?

Asgari Ücret 2025 - Asgari Ücret Ne Kadar?

Vergi Dilimleri 2025

Vergi Dilimleri 2025

-

GİB: e-SMM Uygulamasına Kayıtlı Olan Mükelleflerin E-Fatura Uygulamasına Geçip Geçmeyeceği Hakkında Duyuru

GİB: e-SMM Uygulamasına Kayıtlı Olan Mükelleflerin E-Fatura Uygulamasına Geçip Geçmeyeceği Hakkında Duyuru

-

VERGİ VE MUHASEBE CEZALARINDAN KORUNMA YOLLARI KİTABI

VERGİ VE MUHASEBE CEZALARINDAN KORUNMA YOLLARI KİTABI

-

2025 Yılı Mali Tatil Uygulaması

2025 Yılı Mali Tatil Uygulaması

-

Türkiye Kripto Varlık Borsalarında Yeni Dönem: MASAK 29 Sıra No.lu Genel Tebliğ Kapsamında Bir Değerlendirme

Türkiye Kripto Varlık Borsalarında Yeni Dönem: MASAK 29 Sıra No.lu Genel Tebliğ Kapsamında Bir Değerlendirme

-

Vergi Kaçırana Hapis Cezası Verilir Mi?

Vergi Kaçırana Hapis Cezası Verilir Mi?

-

Yıllık İzinde Yapılan Hata İçin Dört Tür İdari Para Cezası

Yıllık İzinde Yapılan Hata İçin Dört Tür İdari Para Cezası

-

Teknoloji Geliştirme Bölgesi İncelemeleri Başladı!

Teknoloji Geliştirme Bölgesi İncelemeleri Başladı!

-

Tam Mükellef Kurumdan Elde Edilen Kar Payı ve Huzur Hakkı Ortak Tarafından Yıllık Beyanname ile Beyan Edilmeli mi?

Tam Mükellef Kurumdan Elde Edilen Kar Payı ve Huzur Hakkı Ortak Tarafından Yıllık Beyanname ile Beyan Edilmeli mi?

-

7464 Sayılı Kanun Kapsamında Konutların Turizm Amaçlı Kısa Süreli Olarak Kiraya Verilebilmesi İçin İzin Belgesi Alan Mükellefler Hakkında

7464 Sayılı Kanun Kapsamında Konutların Turizm Amaçlı Kısa Süreli Olarak Kiraya Verilebilmesi İçin İzin Belgesi Alan Mükellefler Hakkında

-

Kazanç Yetersizliği Nedeniyle İndirim Konusu Edilemeyen Nakdi Sermaye Tutarının Sonraki Dönemlere Devri

Kazanç Yetersizliği Nedeniyle İndirim Konusu Edilemeyen Nakdi Sermaye Tutarının Sonraki Dönemlere Devri

-

Mali Tatil 1-20 Temmuz 2025 Tarihleri Arasında Uygulanıyor

Mali Tatil 1-20 Temmuz 2025 Tarihleri Arasında Uygulanıyor

-

Yılın Kampanyası: Muhasebecilere Özel Web Sitesi 1.249 TL + KDV